One of the key criteria to buying a home is to have a deposit & enough money to cover your stamp duty and legal fees, if you already own a property hopefully there’s enough equity to draw upon to cover your new purchase, or, perhaps you’re considering selling to release the equity that way.

But if you don’t already own a property Its really, really tough to save for a deposit when you’re paying rent, don’t you agree?

Genuine savings are best

In nearly all cases lenders are looking for a reliable savings history, over at least 3 months, showing that you don’t spend everything you earn and you can meet a commitment which is going to be hundreds of dollars a week. We call this genuine savings, and if you have 5% of the purchase price showing & you can come up with the other costs involved – you could be in business now.

TIP Ideally these savings should be in a separate account for ease for the lender, smaller regular deposits beats larger irregular deposits.

Sale of assets & you’re paying rent

In other cases, if you have the money via sale of an asset or from additional repayments on a personal loan, or perhaps a gift, then we could show your regular commitments via a solid rental payment history (in the exact same name as the applicants) over 12 months.

Larger deposit

There are lenders who are less concerned about how you got the money together (although they don’t like it being borrowed money), but if you have 10% deposit or more then there could be options without requiring this history.

Perhaps there are some options you didn’t know about.

Help from parents via a gift

If you have generous parents & they’re willing to help you beat the price growth, consider taking their assistance. Again, we would prefer this to be 10% or more plus enough to cover your costs, or the lenders are going to want you to show your ability to save as per the above.

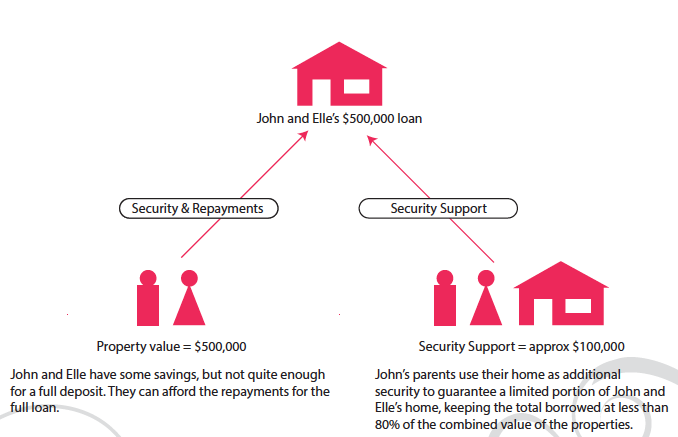

Help from your parents via a limited guarantee

MASSIVELY popular right now! Most parents really want to help their kids get started but perhaps they don’t have the cash – and it might be preferable to having you move back home with them!

Basically in these instances the parents offer their property for a “limited guarantee”, usually around 25% of the value of your home, which is secured against their home and avoids you having to get any money together at all – or you can reduce the guarantee by including your savings.

Now, the negatives – it’s a mortgage against your parents home, so you’re risking their home as well as your own (and future Christmas dinners) if you stop making the repayments. What happens in this instance is your place will be sold and if there’s still a shortfall after the mortgage, legal fees and agents fees are covered the lender will ask your parents to make the repayments on any balance owing, and if they cant – the lender can sell their home to cover the mortgage. Its not pretty so we wont be going there – agreed?

It only works where there’s enough equity to keep mum and dads loan + a buffer + your loan under 80% of the value of their home, we figure this out for you.

The plus is, there’s no need to keep saving, you can get in sooner and hopefully avoid a rising housing market

You avoid lenders mortgage insurance, which can be costly

And the guarantee can be lifted in time, either when your loan is now under 90% of the property value (so you’ve paid some off and the market has done its job too) and you can refinance & pay a smaller mortgage insurance fee – or – when your loan is now 80% of the value of the property and you can complete some forms and you’re done! (Some fees too, but nothing to worry about). Lenders will never initiate this process but keep an eye on your local market and you will know when the time is right.

So the point to note is:

- Its not a a guarantee for the full balance of your loan

- Its not for the full 30 year term

- There’s not a lot for the guarantor to do – complete some forms and get some independent legal advice

- You could be ready to go right now!

Now, be mindful there are a couple of lenders who do this very well – and others that don’t. Ask us for a fact sheet to help you start the conversation and assessment to see if you could qualify right now!