I have a file on my desk right now, and it’s a pretty typical file – straight up and down mum and dad with a couple of kids.

- She’s on maternity leave so they have a little bit of help in family tax benefit.

- He’s putting in some long hours to keep the family financial (and in saying this I am NOT underestimating the long hours mum puts in, never!)

- They have minimal debts, they save, they keep on top of things, they’re actually doing really well.

They’ve outgrown their home and looking to upgrade and contact me to see IF they can do just this. And they can, but here’s the funny thing:

If they walk in the door of every bank on high street they will get a very (very) different response as to how much they can borrow. Huge. So much so that if you walked into only one you might be stuck in the home you’ve overgrown. Fortunately they came to me.

Lets take a look:

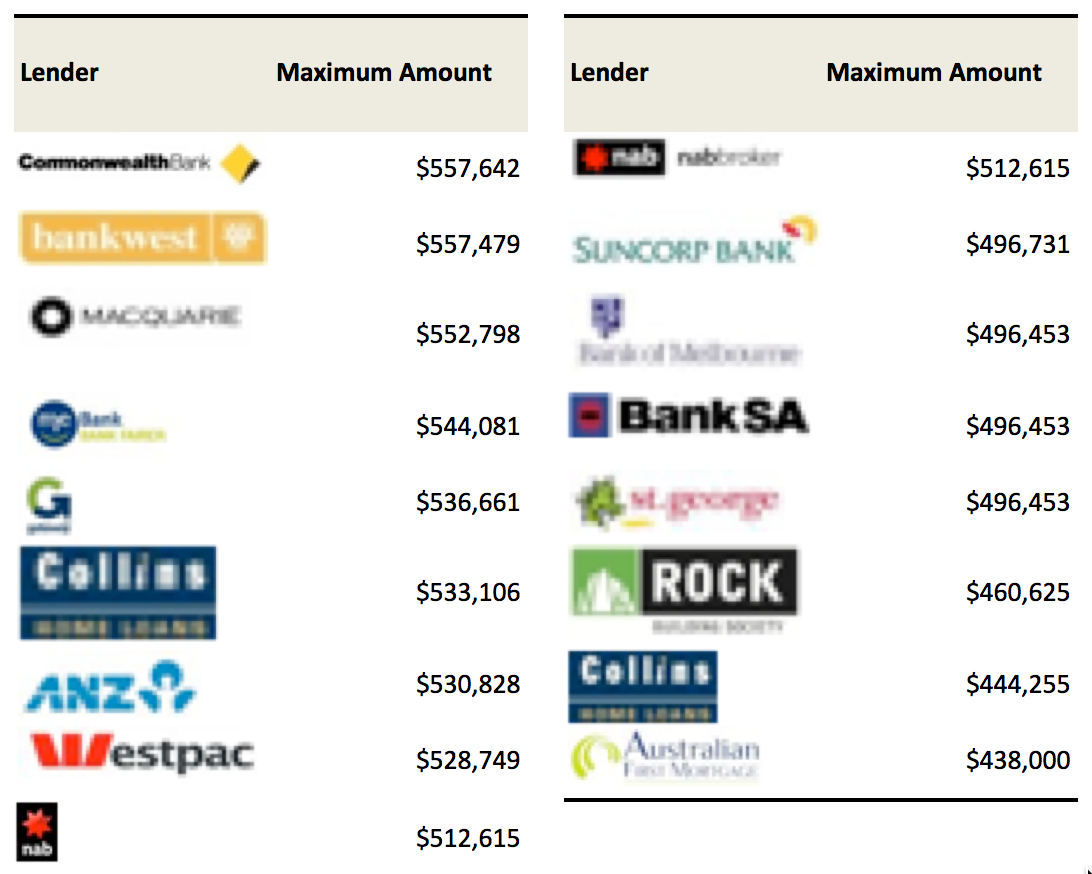

What a difference huh! More than $100,000 difference. Now assuming you’re completely comfortable with the repayments what kind of difference would being able to borrow another $100,000 make to the home you are able to buy?

And it’s not safe to assume that you can simply march into the one on the top of the list – in this case Commbank – and know you’re in the right spot. This is another couple – see they have even more lenders (and a more dramatic difference, just shy of $250,000 difference!) and Commbank doesnt even make the first half of the list.

So, why so different?

All lenders work on a basic framework

- Your net income (after tax income),

- less, your basic living expenses (and this varies based on your household, where you live and the lender’s benchmarks)

- less, your current repayments (and these are treated differently)

- less, extra fixed expenses you need to allow for like child care and foxtel

- What’s left over is called your “net disposable income” and they’ll take a percentage of this (20%, 30%, 40%, 50%, depending on lender) and thats how much they’ll allow you to use for repayments.

- Then, they work backwards, applying their own set of criteria to work out your loan amount.

Confused? I am, but luckily I have a quick and easy calculator to allow me to work this out.

The criteria behind the scenes is very different for each lender:

- Some take family tax benefit as income, some don’t, and some take it but only until your child is age 11

- Some will allow the extra tax break you get for investing

- Some average your income, some take bonuses, some take commission and overtime…. the sky is the limit.

Knowing all about this is a full time job. My full time job!

Lets file this one under you have almost no chance of walking in the door of your bank and getting approved (to do what you want to do).